Favorable individual federal income tax rates established by the Tax Cuts and Jobs Act (TCJA) are scheduled to expire at the end of 2025. But some analysts think that they could be repealed sooner, depending on the results of next year’s presidential election and the preference for budget-neutral government spending. So, taxpayers may want to consider strategies to take advantage of TCJA-related tax breaks as soon as possible.

One tax saving strategy for private business owners to consider is redeeming corporate stock under today’s relatively favorable individual federal income tax rate structure. In a corporate stock redemption, your company buys back some or all of your stock for cash.

These transactions convert theoretical shareholder wealth into cash, but they can result in significant tax consequences for shareholders. Here’s how corporate stock redemptions are treated for federal income tax purposes.

C Corporation Basics

The general rule is that cash payments by a C corporation to redeem shares are classified as corporate distributions to the recipient shareholder. However, the tax rules are tricky.

Stock redemption payments that are classified as corporate distributions are treated as:

1.Taxable dividends. This treatment applies to the extent that your corporation has current or accumulated earnings and profits (E&P). E&P is a tax accounting concept that’s similar to the financial accounting concept of retained earnings.

2.Reduction in your tax basis in the redeemed shares. This treatment applies once your company’s E&P has been exhausted.

3.Capital gain. Once your basis in the redeemed shares has been exhausted, any remainder is treated as a long- or short-term capital gain depending on how long you’ve owned the redeemed shares.

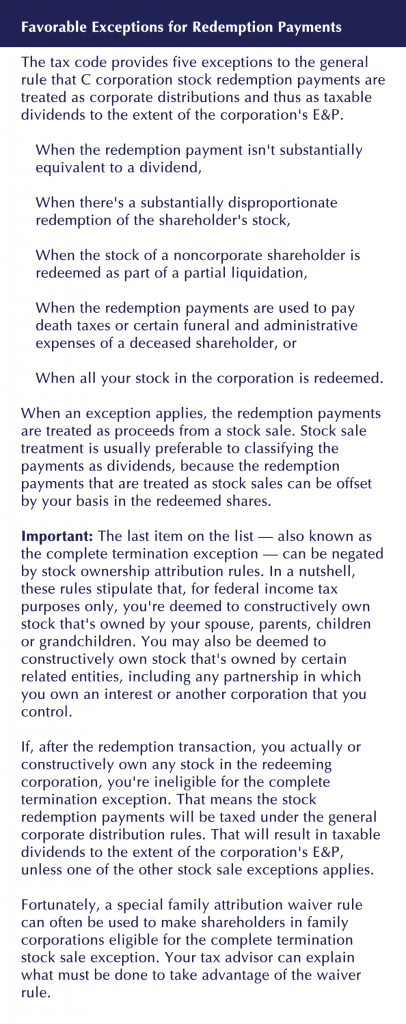

The corporate distribution treatment applies unless an exception is available. (See “Favorable Exceptions for Redemption Payments” below.) When an exception applies, the redemption payments are treated as proceeds from a stock sale. With a stock sale, you recognize a capital gain or loss equal to the difference between the redemption payments and the basis of the redeemed shares.

If you don’t have any significant basis in the redeemed shares or any significant capital losses, there’s usually only a minor distinction between distribution treatment and stock sale treatment under today’s individual federal income tax rate structure. That’s because both dividends and long-term capital gains are currently taxed for high-income taxpayers at the same maximum federal rate of 23.8% (the 20% maximum rate for long-term capital gains and qualified dividends + 3.8% for the net investment income tax or NIIT).

So, individual C corporation shareholders will get favorable federal income tax treatment for stock redemption payments received in 2019, even if they’re treated as corporate distributions. The tax treatment of stock redemption payments received in future years may not be nearly as favorable.

S Corporation Basics

When an S corporation redeems an owner’s stock, stock sale treatment applies, unless the S corporation has E&P from an earlier period as a C corporation. If the S corporation has E&P, corporate distribution treatment applies, and the rules get more complicated.

When corporate distribution treatment applies, all or part of the redemption payments can potentially be treated as taxable dividends (to the extent of the corporation’s E&P). However, if an exception is available, stock sale treatment will apply even if the S corporation has E&P. (See “Favorable Exceptions for Redemption Payments” below.)

Timing Issue

To help minimize the taxes you’ll owe on payments from a corporate redemption, consider redeeming your shares sooner, rather than later. Higher maximum federal income tax rates on both dividends and long-term gains could take effect in future years.

Of particular concern is the risk that the maximum federal rate on redemption payments classified as dividends could be increased to equal the maximum rate on ordinary income. In 2017, the maximum ordinary income rate was 39.6% plus another 3.8% for the NIIT. Depending on political developments, the ordinary income rate could be increased even higher than this level.

Bottom Line

Under current law, the following maximum federal rates apply to individual recipients of stock redemption payments made in 2018 through 2025:

•23.8% (20% + 3.8% NIIT) on payments treated as dividends, and

•23.8% (20% + 3.8% NIIT) on the taxable portion of payments treated as long-term capital gains.

It’s possible that a new president and a new Congress could hike these rates long before 2026.

Therefore, waiting to redeem shares could trigger a bigger tax bill for you. This risk must be balanced against the fact that 2019–2020 redemptions will trigger current tax liabilities versus deferred tax liabilities if you defer a redemption to a future year. Talk with your tax advisor as soon as possible if you’re interested in the stock redemption strategy.

© Copyright 2019 Thomson Reuters. All rights reserved. Republication or redistribution of Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. Thomson Reuters and the Kinesis logo are trademarks of Thomson Reuters and its affiliated companies.

Disclaimer of Liability

Our firm provides the information in this e-newsletter for general guidance only, and does not constitute the provision of legal advice, tax advice, accounting services, investment advice or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal or other competent advisors. Before making any decision or taking any action, you should consult a professional advisor who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this e-newsletter are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability and fitness for a particular purpose.

Blog

Nonprofit Insights