When a loved one who was “financially comfortable” passes away, his or her family must deal with the emotional issues that come with the loss — as well as winding up the decedent’s financial affairs.

Surviving family members are often unprepared for the tax issues that may arise when a loved one dies. Here’s some guidance to help you manage important tax and financial considerations during this difficult time.

Pay Special Attention to Final Medical Expenses

If large uninsured medical expenses were accrued, but not paid, before death, the executor must make a potentially important choice about how they’re treated for federal tax purposes.

The executor can choose to deduct accrued (as-yet-unpaid) medical expenses, along with any medical expenses paid before death, on the decedent’s final Form 1040. These medical expenses are deductible to the extent they exceed 10 percent of AGI for 2019 (up from 7.5 percent of AGI for 2018), assuming the decedent’s final Form 1040 claims itemized deductions.

To take advantage of this special rule, the accrued medical expenses must be paid out of the decedent’s estate during the one-year period beginning with the day after the date of the decedent’s death.

This special rule is an exception to the general rule that expenses of a cash-basis taxpayer must be paid in cash before they can be deducted. Final medical expenses can easily exceed the percent-of-AGI threshold, especially when death occurs early in the year before much income has been earned.

There’s another option for wealthy individuals with estates above the unified federal estate and gift tax exemption amount: The executor can choose to deduct accrued medical expenses on the decedent’s federal estate tax return, rather than on the decedent’s final 1040.

When federal estate tax is owed, deducting accrued medical expenses on the estate tax return is usually the better option. That’s because the estate tax rate is 40 percent, while the decedent’s final federal income tax rate could be as low as 10 percent. Moreover, the full amount of accrued medical expenses can be deducted on the estate tax return (not just the amount that’s over the percent-of-AGI threshold).

Important note: Under the Tax Cuts and Jobs Act (TCJA), the unified federal estate and gift tax exemption is $11.4 million per person for 2019 (up from $11.18 million for 2018). For married couples, the exemption is effectively doubled to $22.8 million for 2019 (up from $22.36 million for 2018). The exemption amounts will be adjusted annually for inflation from 2020 through 2025. In 2026, the exemption is set to return to an inflation-adjusted $5 million, unless Congress extends the more generous exemption.

Role of the Executor

When a loved one passes away, someone must handle the resulting tax issues. That person may be identified in the decedent’s will as the “executor” of the decedent’s estate. If there’s no will, the probate court will appoint an administrator. In either case, we’ll refer to that person as the executor for purposes of this article.

The executor is responsible for:

•Identifying the estate’s assets,

•Paying off the estate’s debts and

•Distributing any remainder to the decedent’s rightful heirs and beneficiaries.

The executor also must file any necessary tax returns and arrange to pay any taxes.

Final Tax Return for Unmarried Decedents

For unmarried decedents, the executor must file a final Form 1040 that covers the period from January 1 through the date of death. The final return is due on the standard date for individuals. (That’s April 15, 2020, for someone who dies in 2019.) The return can be extended for six months, to October 15 (adjusted for weekends and holidays) of the year after the year of death.

Joint Returns for Surviving Spouses

The tax filing requirements are different for married decedents. If the surviving spouse remarries on or before December 31 of the year of the decedent’s death, married-filing-separate status must be used for the decedent’s final Form 1040.

However, when the surviving spouse remains unmarried as of the end of the year during which the decedent passes away, the final Form 1040 can be a joint return prepared as if the decedent were still alive. This final joint return includes the decedent’s income and deductions up to the time of death, plus the surviving spouse’s income and deductions for the entire year.

Filing a joint return is usually beneficial, because it allows the surviving spouse to take advantage of the more taxpayer-friendly rates and rules that apply to married couples who file joint tax returns.

In addition, the joint-filer tax rates are extended to a surviving spouse who is a qualified widow or widower for the two tax years following the year of the death of the deceased spouse. To qualify for this extension for a particular tax year, the surviving spouse must:

•Be unmarried as of the end of that year,

•Pay more than half the cost of maintaining a home that’s the principal home for the entire year of a child of the surviving spouse (including a stepchild) who qualifies as a dependent of the surviving spouse and

•Have been eligible to file a joint return with the decedent for the tax year during which the decedent passed away.

Important note: The Tax Cuts and Jobs Act (TCJA) suspended dependent exemption deductions for 2018 through 2025. However, for purposes of various provisions that refer to individuals for whom dependent exemption deductions are allowed (such as the eligibility rule for qualified widow or widower status), a dependent exemption (of $0) is still deemed to exist for 2018 through 2025.

Decedents with Revocable Trusts

To avoid probate, some individuals and married couples set up revocable trusts to hold valuable assets, including real property and financial accounts. Revocable trusts may also be called living trusts or family trusts.

For tax purposes, as long as the trust remains in revocable status, it’s considered a grantor trust and its existence is disregarded for federal tax purposes. Therefore, the grantor or grantors are treated as still personally owning the trust’s assets for tax purposes, and tax returns of the grantor(s) are prepared accordingly.

Unmarried decedents. When an unmarried individual passes away, his or her grantor trust becomes irrevocable. As such, the trust will be treated as a separate taxpayer that’s subject to the federal income tax rules for trusts.

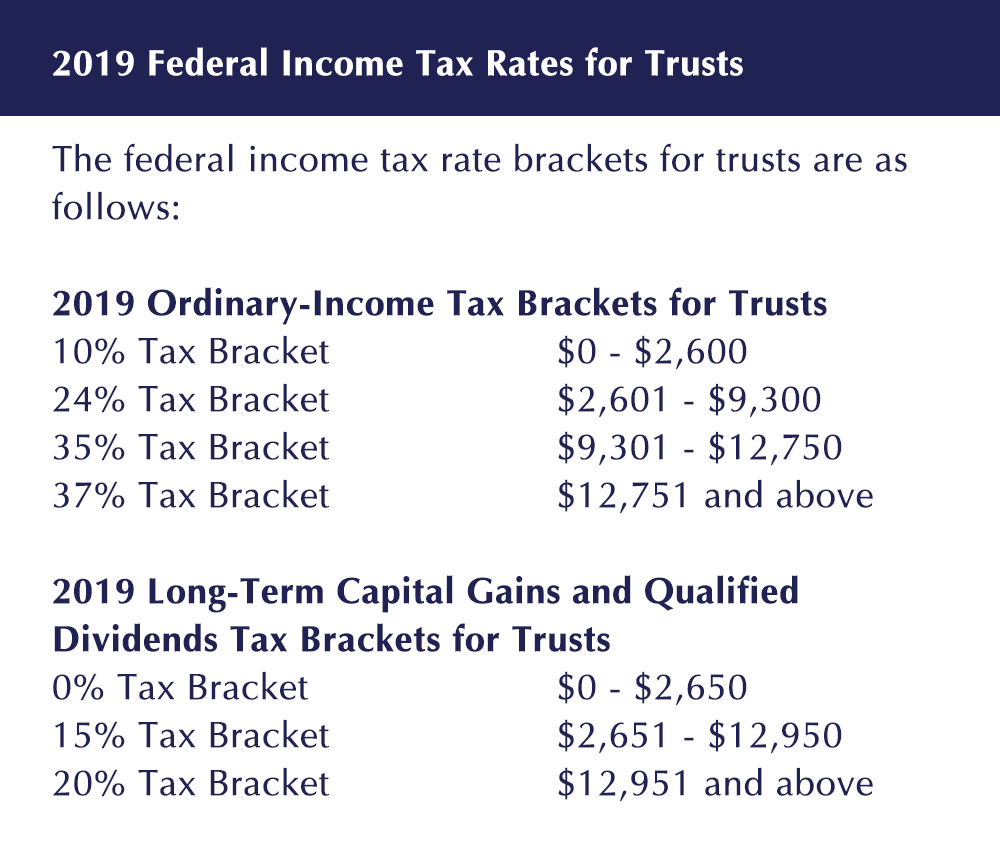

This is an unfavorable development, because the tax rates on undistributed trust income quickly climb to the maximum 37 percent rate for ordinary income and short-term capital gains and the maximum 20 percent rate for long-term capital gains and qualified dividends. (See “Federal Income Tax Rates for Trusts” below.) If the 3.8 percent net investment income tax also applies, the marginal federal rate on a trust’s undistributed investment income and gains can be as high as 40.8 percent or 23.8 percent.

Married decedents. Grantor trusts set up by married couples typically continue to exist as such when the first spouse passes away. In that case, the trust’s existence continues to be disregarded for federal tax purposes, and the surviving spouse’s tax returns are prepared without regard to the trust.

However, when the surviving spouse eventually passes away, the grantor trust becomes an irrevocable trust. As such, it is treated as a separate taxpayer with the aforementioned unfavorable federal income tax consequences.

Important note: Your tax advisor can help you plan to minimize exposure to the high federal income tax rates for trusts. How? The trust can be drained of income and gains by distributing them to the trust beneficiaries, or the trust can be liquidated by distributing its assets to them.

Need Help?

In life, two things are certain: death and taxes. Ultimately, you can’t escape death, but smart planning can help minimize taxes.

Whether you’re married or single, everyone needs an estate plan — even if it’s just a will — to help surviving family members wind up decedents’ financial affairs after they’re gone. A tax professional can help you plan for the inevitable, while you’re still alive.

On the flip side, if you’ve lost a loved one, it’s important to contact a tax professional promptly to put your mind at ease. This article barely scratches the surface of the potential tax issues that may arise. A tax advisor can explain important tax considerations based on the decedent’s unique situation and help the executor comply with applicable federal and state tax rules.

Contact us at 434.296.2156 or info@hwllp.cpa for more information.

© Copyright 2019 Thomson Reuters. All rights reserved. Republication or redistribution of Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. Thomson Reuters and the Kinesis logo are trademarks of Thomson Reuters and its affiliated companies.

Disclaimer of Liability

Our firm provides the information in this e-newsletter for general guidance only, and does not constitute the provision of legal advice, tax advice, accounting services, investment advice or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal or other competent advisers. Before making any decision or taking any action, you should consult a professional adviser who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this e-newsletter are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability and fitness for a particular purpose.

Blog

Nonprofit Insights