The COVID-19 pandemic has led to many shifts in the way we operate our affairs. We do things today we had not even considered in the past. This applies to the way we shop, spend time with friends, and conduct our businesses. Undoubtedly, the far-reaching impacts of the pandemic have many companies asking new questions when it comes to their financial reporting. Our team is here to help you as you cover this new terrain. The following is a list of six questions and the answers businesses will now need to address in order to prepare their financial reports.

Q1: How do I report the incremental expenses (such as additional sanitizing supplies, masks, temporary hazard pay to employees, etc.) incurred in response to the COVID-19 pandemic on the income statement?

A1: These incremental expenses would most likely be considered unusual or infrequent under U.S. Generally Accepted Accounting Principles (GAAP). U.S. GAAP requires these expenses, if material, be classified separately as a component of ordinary income or loss, “above the line.” The nature and effect should be disclosed either on the face of the income statement or in a note (FASB ASC 220-20-45 and 220-20-50).

Q2: How do I record the Paycheck Protection Program (PPP) loan proceeds and forgiveness?

A2.1: Not-for-profit organizations can record the loan proceeds as debt or as a conditional grant, depending on whether or not they expect the loan to be forgiven. It’s always acceptable to record the PPP loan as debt (FASB ASC 470) and then to write off the debt when it is legally forgiven by the bank. The forgiven amount would then be shown as other income on the statement of activities. If the nonprofit organization believes the loan will be forgiven, it could treat the transaction as a government grant liability (conditional grant) and then reclassify the liability to income as the expenses are incurred (FASB ASC 958-605).

A2.2: For-profit companies have four options on how to handle the PPP loan:

- Debt (FASB ASC 470) – Companies can write off the debt when the loan is legally forgiven by the bank. It is always acceptable to use this method.

- Government grant under FASB ASC 958-605 – U.S. GAAP does not provide direct guidance for a company receiving a government grant. However, U.S. GAAP does allow a company to look for similar transactions or events within U.S. GAAP and then to consider nonauthoritative guidance from other sources (FASB ASC 105-10-15-2). Because of this, for-profit companies can analogize the U.S. GAAP guidance provided for nonprofits receiving government grants, which allows the entity to write off the debt to income as the expenses are incurred if management believes that the probability threshold is high enough that the debt will be forgiven, i.e., the conditions are substantially met.

- Government grant under International Accounting Standards 20 (IAS 20), Accounting for Government Grants and Disclosure of Government Assistance – Since the IAS 20 provides guidance for companies receiving government grants, management can analogize to IAS 20 and write off the debt to either income or as a reduction of related expenses as the expenses are incurred when there is “reasonable assurance” the debt will be forgiven.

- Gain contingency (FASB ASC 450-30) – The PPP loan proceeds are recorded as income once all uncertainties regarding the final forgiveness of the loan have been resolved.

Q3: How do I account for the PPP loan if I expect only a portion of the loan to be forgiven?

A3: As of now, you will have to account for the PPP loan in its entirety using one of the accounting policies noted above. You cannot bifurcate the PPP loan to account for a portion as debt and a portion as something else. Let’s look at some examples under the most likely scenarios:

- If your accounting policy is to treat the PPP loan as debt, you will record the loan proceeds as a note payable and accrue interest just like any other loan. Then you will remove the forgiven amount from the PPP loan liability and report it as other income on the income statement when the debt is legally forgiven. The remaining debt and accrued interest will be paid down over the term of the loan.

- If your accounting policy is to treat the PPP loan as a conditional grant (such as under FASB ASC 958), you will record the loan proceeds as a refundable grant liability. That liability will be reduced and reclassified to other income on the income statement when the PPP allowable expenses are incurred. The amount left over will be removed from the refundable grant liability as the funds are repaid to the bank. It is not shown as a note payable. Interest will be accrued for the portion of the proceeds that the organization expects to repay to the bank. Disclosures will be important so that financial statement users understand the nature of the grant liability and any repayment terms.

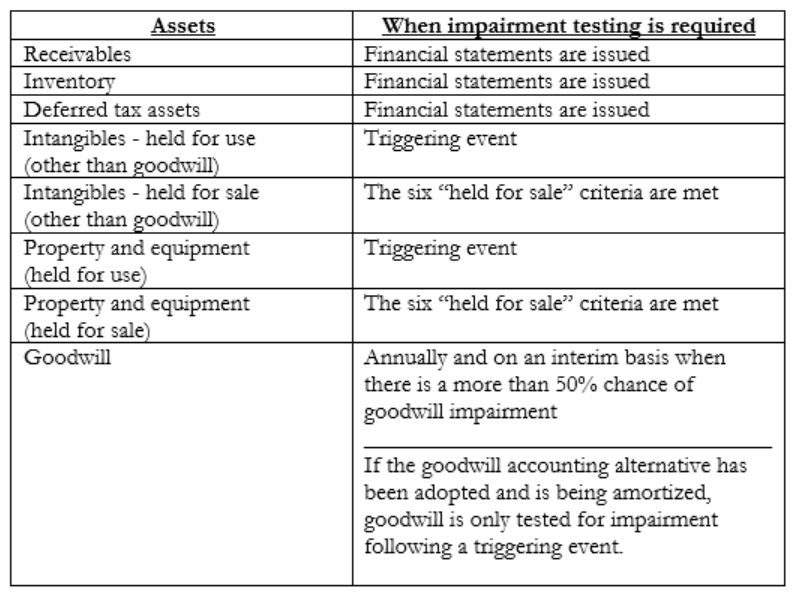

Q4: Could the impact of COVID-19 require my organization to test certain assets for impairment?

A4.1: Yes, the impact of COVID-19 may trigger certain assets to be tested for impairment, but keep in mind that some assets are required to be tested regardless of the negative economic impact of the pandemic. See chart below.

A4.2: If assets are impaired, additional disclosures are required.

Q5: Could the COVID-19 pandemic impact my inventory costing?

A5: Yes, manufacturing entities will need to assess their production capacity to determine if there is an impact on costing. To prevent ending inventory from being overstated due to abnormally low production, U.S. GAAP requires the allocation of fixed production overhead be based on the NORMAL capacity of the production facilities. According to FASB ASC 330-10-30-6, “The amount of fixed overhead allocated to each unit of production shall not be increased as a consequence of abnormally low production or idle plant.”

Q6: Could the negative economic impact of COVID-19 require my company to make going concern disclosures in our financial statements?

A6: Yes, U.S. GAAP requires management to assess going concern when financial statements are issued (FASB ASC 205-40). For some organizations, the negative economic impact resulting from COVID-19 qualifies as an event or condition that raises substantial doubt about the ability of the organization to continue as a going concern. Once that threshold is reached, disclosures need to be added to the financial statements, even if management believes their plans to mitigate the threat can be effectively implemented and will work. Other disclosures are required if management believes their plans will not alleviate the going concern threat.

Many factors you need to consider in your accounting today did not exist a year ago, but our team has the solutions you need. If you have further questions or would like to discuss your specific accounting needs, contact us today.

Contact Us

Disclaimer of Liability

Our firm provides the information in this article for general guidance only, and does not constitute the provision of legal advice, tax advice, accounting services, investment advice or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal or other competent advisors. Before making any decision or taking any action, you should consult a professional advisor who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this blog are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability and fitness for a particular purpose.

Blog

Nonprofit Insights