The IRS and employers often are at loggerheads over the classification of workers as employees or independent contractors. Typically, many employers want to treat workers as independent contractors, while the IRS often determines that workers are misclassified employees. Sometimes, the issue winds up in the courts.

Fortunately, there might be a way for employers to obtain a measure of protection if the IRS challenges the classification of a worker or workers. With “Section 530 relief,” an employer may avoid adverse tax consequences from a misclassification of employment status. However, this special safe-harbor rule is only available if the employer can show it had a reasonable basis for treating workers as independent contractors.

Background Information

Make no mistake about it — the stakes are high for employers. Let’s start with the payroll tax aspects.

If a worker is treated as an employee rather than an independent contractor, the employer must withhold federal income tax and the employee’s share of Old Age Survivors Disability Insurance (OASDI) tax, commonly called “Social Security tax,” plus the employee’s share of Hospital Insurance (HI) tax, also called Medicare tax. In addition, the employer must pay the employer’s share of the taxes and the federal unemployment tax (FUTA). The employer must also issue Form W-2 for the wages and send a copy to the IRS.

The dollar amount of these payroll taxes keep going up. For 2020, the “Social Security wage base” for purposes of the OASDI tax is $137,700, up from $132,900 in 2019. The tax rate for OASDI tax remains 6.2%. As before, the 1.45% HI tax continues to apply to all wages paid to employees.

For example, suppose a worker expects to earn $150,000 in 2020. The OASDI portion of the tax will be $8,537.40 (6.2% of $137,700) and the HI portion will be $2,175 (1.45% of $150,000). Thus, the total comes to $10,712.40. This is the amount both the employee and the employer have to pay.

And that’s not the end of the story. Employers may also be responsible for certain state taxes. What’s more, if a worker is classified as an employee, he or she may be eligible for expensive fringe benefits, such as health insurance and 401(k) matching contributions.

When you multiply these amounts for a sizeable workforce, it’s no wonder that employers frequently want to classify workers as independent contractors. But if an employer improperly classifies employees as independent contractors, it could be hit with a significant tax bill for unpaid employment taxes, interest and penalties.

Volumes have been written about the distinctions between independent contractors and employees. Essentially, one of the key factors is that if you have little or no control over the way a worker gets the job done, he or she is an independent contractor. Conversely, if you have the legal right to control how the worker performs a job, he or she is an employee — even if you don’t actually exercise that right.

Despite these general guidelines, employers and the IRS often agree to disagree about the classification of workers. This is where Section 530 can come into play.

How Section 530 Works

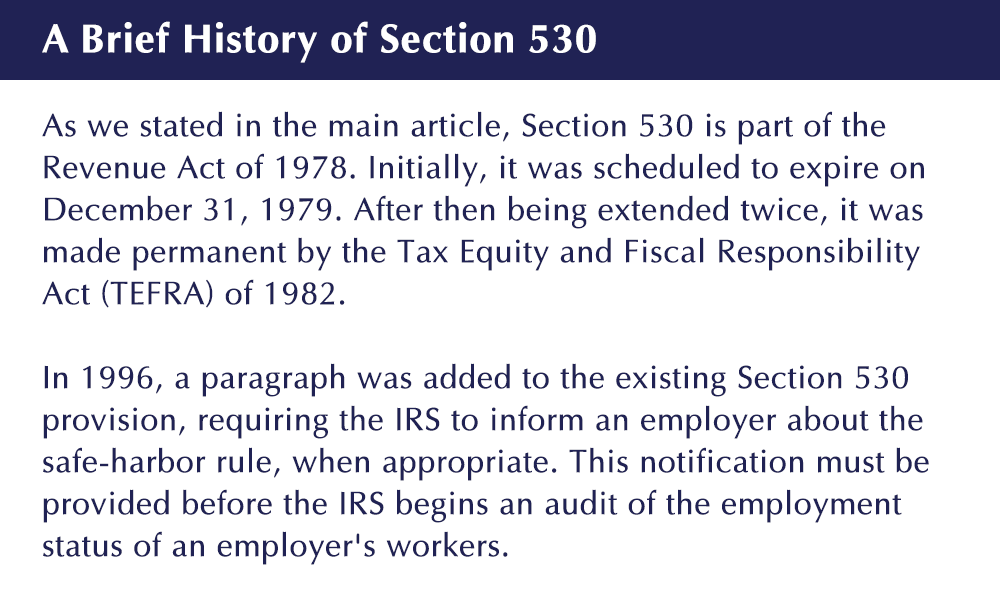

The Section 530 safe-harbor rule may be invoked when a business is assessed back taxes and penalties for misclassifying workers as independent contractors instead of employees. It’s often assumed that the name is taken from a section of the Internal Revenue Code, but it actually stems from Section 530 of the Revenue Act of 1978, the source of this provision.

Congress enacted Section 530 of the 1978 law to provide relief from potentially large retroactive employment tax assessments for taxpayers who had acted in good faith. According to some tax commentators, it was also intended to curb the IRS’s overly aggressive enforcement of employment tax laws. In any event, the provision was supposed to be temporary in nature, but the safe-harbor rule has endured for decades and continues to be a fallback position involving worker classification controversies to this day (see box below).

In a nutshell, if a business can show it had a reasonable basis for treating workers as independent contractors, the resulting back taxes, fines and penalties may be waived. Therefore, it is essential that you obtain the services of a tax professional before you enter into any agreements with the IRS.

There are three main requirements for securing Section 530 relief.

1. Reasonable basis. An employer must have a “reasonable basis” for treating workers as independent contractors, rather than employees. This might be established by one of the following:

- A related court case or IRS ruling.

- A prior IRS audit involving examination of employment taxes at a time when the employer treated similar workers as independent contractors and there was no IRS reclassification of these workers.

- If a significant segment of the employer’s industry treats similar workers as independent contractors.

- If the employer is relying on some other reasonable authority (for example, the opinion of an attorney or accountant familiar with the business operation).

2. Employment status consistency. In the past, the employer has only treated the workers and any similar workers as independent contractors. There is no exception.

3. Reporting consistency. At all times, the employer has filed all federal tax returns consistent with your treatment of the workers as independent contractors. For instance, your business must have provided workers with Form 1099s and not W-2s.

ALL of these three requirements must be met. A single failure is fatal to your claim.

Finally, if you aren’t sure you are correctly treating workers as independent contractors, contact us to help you make a determination. This is one area where your business can’t afford to make any mistakes. If you are contacted by the IRS, we can also provide guidance on applying the Section 530 safe-harbor rule to your situation. Fill out the form following “A Brief History” below and we’ll contact you.

Contact Us

© 2024 CPA Site Solutions.

Disclaimer of Liability

Our firm provides the information in this article for general guidance only, and does not constitute the provision of legal advice, tax advice, accounting services, investment advice or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal or other competent advisors. Before making any decision or taking any action, you should consult a professional advisor who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this blog are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability and fitness for a particular purpose.

Blog

Nonprofit Insights